BOJ 펴서 먹고 인생 피긴 힘들지.

이보단,

S&P를 주목하고 있었는데. 유일하게 악재가 될 수 있는 상황은 밤중에 발표되는 GDP.

GDP 발표 후 가능한 시장 시나리오는

1. 급등

2. 급락

3. 지지부진

1. 금등 -> 못들어감

2. 급락 -> 못들어감

3. 지지부진 -> 불확실 해소. "롱".

20160129. 3번.

2016년 1월 31일 일요일

Some articles : Twosigma, Machine Learning

1. http://www.businessinsider.com/artificial-intelligence-team-at-bridgewater-2015-2

2. http://qz.com/389647/artificial-intelligence-is-the-next-big-thing-for-hedge-funds-seeking-an-edge/

3. http://www.forbes.com/sites/nathanvardi/2016/01/13/top-quant-hedge-funds-stand-out-with-good-2015/#3a6dcf96558e

4. http://www.forbes.com/sites/nathanvardi/2015/09/29/rich-formula-math-and-computer-wizards-now-billionaires-thanks-to-quant-trading-secrets/#41c08ff57f30\

5. http://www.wired.com/2016/01/the-rise-of-the-artificially-intelligent-hedge-fund/

6. http://www.valuewalk.com/2016/01/managed-futures-market-turmoil/

7. http://marketsmedia.com/best-hedge-fund-two-sigma-investments/

머신러닝개괄 쉽게 설명 한글

2. http://qz.com/389647/artificial-intelligence-is-the-next-big-thing-for-hedge-funds-seeking-an-edge/

3. http://www.forbes.com/sites/nathanvardi/2016/01/13/top-quant-hedge-funds-stand-out-with-good-2015/#3a6dcf96558e

4. http://www.forbes.com/sites/nathanvardi/2015/09/29/rich-formula-math-and-computer-wizards-now-billionaires-thanks-to-quant-trading-secrets/#41c08ff57f30\

5. http://www.wired.com/2016/01/the-rise-of-the-artificially-intelligent-hedge-fund/

6. http://www.valuewalk.com/2016/01/managed-futures-market-turmoil/

7. http://marketsmedia.com/best-hedge-fund-two-sigma-investments/

머신러닝개괄 쉽게 설명 한글

http://slownews.kr/41461

2016년 1월 24일 일요일

Some articles and papers

1. The best strategies we have tested

- http://www.quant-investing.com/strategies

2. Does the "Sharp Parity" work better than "Risk Parity"?

- http://blog.alphaarchitect.com/2015/01/27/does-sharpe-parity-work-better-than-risk-parity/?utm_source=Alpha%20Architect%20Website%20Users&utm_campaign=df7ac0889d-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_2f87b7924e-df7ac0889d-188292261#.VMlTH2tdaK0

3. A Tug of war : Overnight Versus Intraday Expected Returns

http://blog.alphaarchitect.com/2015/02/12/overnight-momentum-vs-intraday-momentum/?utm_source=Alpha%20Architect%20Website%20Users&utm_campaign=72df424a39-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_2f87b7924e-72df424a39-188292261#.VOAT8ZWGkEN.facebook

4. Global Assets Allocation - New Books!

http://mebfaber.com/2015/02/24/global-asset-allocation-a-survey-of-the-worlds-top-asset-allocation-strategies/

5. How to combine value and momentum investing strategies

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

6. 9 Mistakes Quant make that cause basctests to lie

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

7. Looking back at Risk Parity's Golden age

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

8. Our thought about risk parity and all weather - Bridgewater capital

https://www.bwater.com/Uploads/FileManager/research/Our%20Thoughts%20about%20Risk%20Parity%20and%20All%20Weather.pdf

9. Two centuries of momentum

https://www.thinknewfound.com/foundational-series/two-centuries-of-momentum/

10. How not to wipe out with momentum

http://www.researchaffiliates.com/Our%20Ideas/Insights/Fundamentals/Pages/448_How_NOT_to_Wipe_Out_with_Momentum.aspx

<Papers>

1. . . . and the Cross-Section of Expected Returns

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2249314

2. Factor investing

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2277397&rec=1&srcabs=2249314&alg=1&pos=2

3. Momentum crash

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2371227#.VcAeLr2pmyY.facebook

4. Quantifying trading behavior in financial markets using google trends

https://www.google.co.kr/search?q=Quantifying+Trading+Behavior+in+Financial+Markets+Using+Google+Trends&oq=Quantifying+Trading+Behavior+in+Financial+Markets+Using+Google+Trends&aqs=chrome..69i57j69i59j69i61l2.437j0j9&sourceid=chrome&es_sm=91&ie=UTF-8

5. Facts about Factor

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2594485

- http://www.quant-investing.com/strategies

2. Does the "Sharp Parity" work better than "Risk Parity"?

- http://blog.alphaarchitect.com/2015/01/27/does-sharpe-parity-work-better-than-risk-parity/?utm_source=Alpha%20Architect%20Website%20Users&utm_campaign=df7ac0889d-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_2f87b7924e-df7ac0889d-188292261#.VMlTH2tdaK0

3. A Tug of war : Overnight Versus Intraday Expected Returns

http://blog.alphaarchitect.com/2015/02/12/overnight-momentum-vs-intraday-momentum/?utm_source=Alpha%20Architect%20Website%20Users&utm_campaign=72df424a39-RSS_EMAIL_CAMPAIGN&utm_medium=email&utm_term=0_2f87b7924e-72df424a39-188292261#.VOAT8ZWGkEN.facebook

4. Global Assets Allocation - New Books!

http://mebfaber.com/2015/02/24/global-asset-allocation-a-survey-of-the-worlds-top-asset-allocation-strategies/

5. How to combine value and momentum investing strategies

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

6. 9 Mistakes Quant make that cause basctests to lie

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

7. Looking back at Risk Parity's Golden age

http://blog.alphaarchitect.com/2015/03/26/the-best-way-to-combine-value-and-momentum-investing-strategies/#.VSGqdy9darV

8. Our thought about risk parity and all weather - Bridgewater capital

https://www.bwater.com/Uploads/FileManager/research/Our%20Thoughts%20about%20Risk%20Parity%20and%20All%20Weather.pdf

9. Two centuries of momentum

https://www.thinknewfound.com/foundational-series/two-centuries-of-momentum/

10. How not to wipe out with momentum

http://www.researchaffiliates.com/Our%20Ideas/Insights/Fundamentals/Pages/448_How_NOT_to_Wipe_Out_with_Momentum.aspx

<Papers>

1. . . . and the Cross-Section of Expected Returns

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2249314

2. Factor investing

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2277397&rec=1&srcabs=2249314&alg=1&pos=2

3. Momentum crash

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2371227#.VcAeLr2pmyY.facebook

4. Quantifying trading behavior in financial markets using google trends

https://www.google.co.kr/search?q=Quantifying+Trading+Behavior+in+Financial+Markets+Using+Google+Trends&oq=Quantifying+Trading+Behavior+in+Financial+Markets+Using+Google+Trends&aqs=chrome..69i57j69i59j69i61l2.437j0j9&sourceid=chrome&es_sm=91&ie=UTF-8

5. Facts about Factor

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2594485

2016년 1월 10일 일요일

2016년 1월 5일 화요일

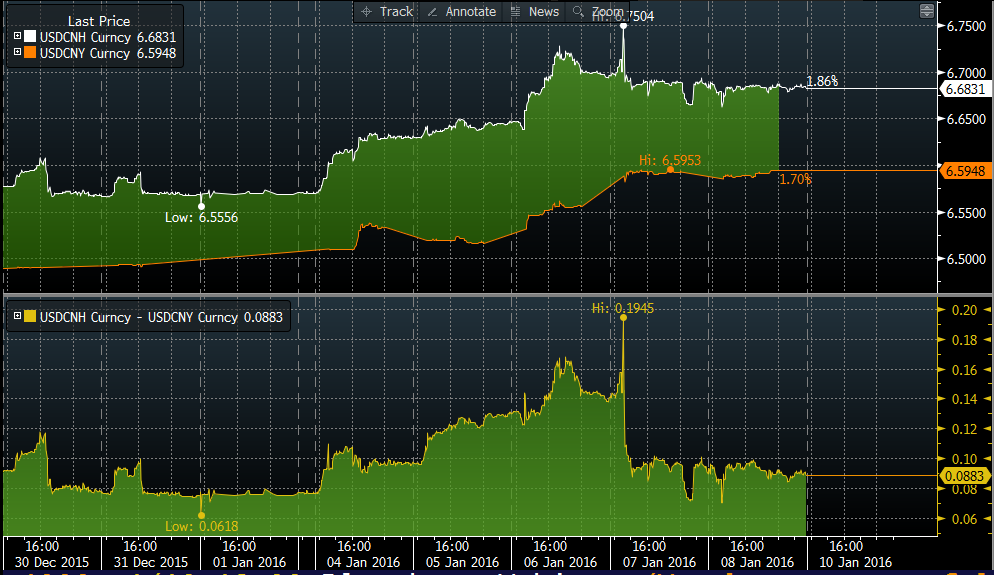

위안화_쓰는중

| 일별 | 달러-위안 기준환율 | 시장거래 환율 마감가 |

| 30일 | 6.4895 | 6.4902 |

| 31일 | 6.4936 | 6.4936 |

| 4일 | 6.5032 | 6.5172 |

| 5일 | 6.5169 | 6.5199 |

| 6일 | 6.5314 | 6.5575 |

이곳 저곳에서 보면 내수 위주로 체질 개선을 해야 한다고 나오는데 롤 모델이 어디지? 그리고 이게 가능한 상태는 어떤 상태 인가?

3. A few small steps for the CNY, potentially a big leap lower in EM FX. The clearest implication of China joining the currency depreciation train is that it further increases depreciation pressures on the rest of the EM FX complex. There are two important channels of transmission here: First, because China as a producer competes with several EMs in global markets, those EM exporters just became a touch less competitive relative to Chinese exporters;

and second because China as a consumer is also a large destination for exports from the rest of EM, although in this case there is at least the possibility of a partial offset from any improvement in demand if an easing in financial conditions is delivered.

So for EMs that have been trying to address their external balance, and have seen depreciating currencies since 2013, some of that relative price shift has just been undone.

And if the recent CNY moves are the start of a journey, even undoing half of the accumulated trade-weighted appreciation of the last three years, this may provoke a meaningful additional bout of currency depreciation across the EM complex (Exhibit 1).

EM currency depreciation 에 큰 영향

1. 몇몇 EM 국가들은 중국과 수출 경쟁에 놓여 있다.

- 위안화 약세로 수출 경쟁 악화

2. 수요자로써 중국의 역할 약화

- 물론 중국 경제가 easing으로 인해 회복 된다면 이에 대한 긍정적인 측면도 있을 것이다.

4. THB, TWD, KRW and MYR most vulnerable to the increased competitiveness of Chinese exports. Digging deeper into the two channels of transmission reveals which EMs could see further FX pressures if the devaluation in China extends.

Regarding the first channel, in the global market for exports China competes with countries that export the same goods, as well as countries that export to the same places.

We use two variants of the Finger and Kreinin (1979) index to identify competition across each of these dimensions based on 2014 data from UNCTAD (the United Nations Conference on Trade and Development) on the bilateral trade of 255 types of goods exported from 50 countries that together comprise roughly 90% of world goods exports (Exhibit 2).

A value of 1 on this index indicates an identical match – countries that are in direct competition based on the category of goods they export or the countries that buy their goods – while 0 indicates a completely dissimilar export basket.

The top right of Exhibit 2 reveals a cluster of countries (THB, TWD, KRW, MYR) that export similar categories of goods to similar markets, and are likely to be most exposed to more competitive Chinese exports.

These are also the currencies where we forecast the most depreciation (along with IDR) in the Asian region. Interestingly, the CEE-3 and TRY, grouped at the bottom right of exhibit 2, export similar categories of goods to China, but to very different markets – so these currencies should be less affected by the CNY depreciation, at least in the short run.

크루그먼

http://krugman.blogs.nytimes.com/2015/08/12/china-bites-the-cherry/?_r=2#

"But it’s important to understand how that works. When Japan loosens money, it creates an incentive to move funds abroad, causing the yen to fall. This process only stops once the yen has fallen enough that investors consider it undervalued, and are willing to buy Japanese securities in the expectation of a future yen rise. Exchange rate overshooting is an essential part of the story."

크루그먼

http://krugman.blogs.nytimes.com/2015/08/12/china-bites-the-cherry/?_r=2#

"But it’s important to understand how that works. When Japan loosens money, it creates an incentive to move funds abroad, causing the yen to fall. This process only stops once the yen has fallen enough that investors consider it undervalued, and are willing to buy Japanese securities in the expectation of a future yen rise. Exchange rate overshooting is an essential part of the story."

피드 구독하기:

글 (Atom)